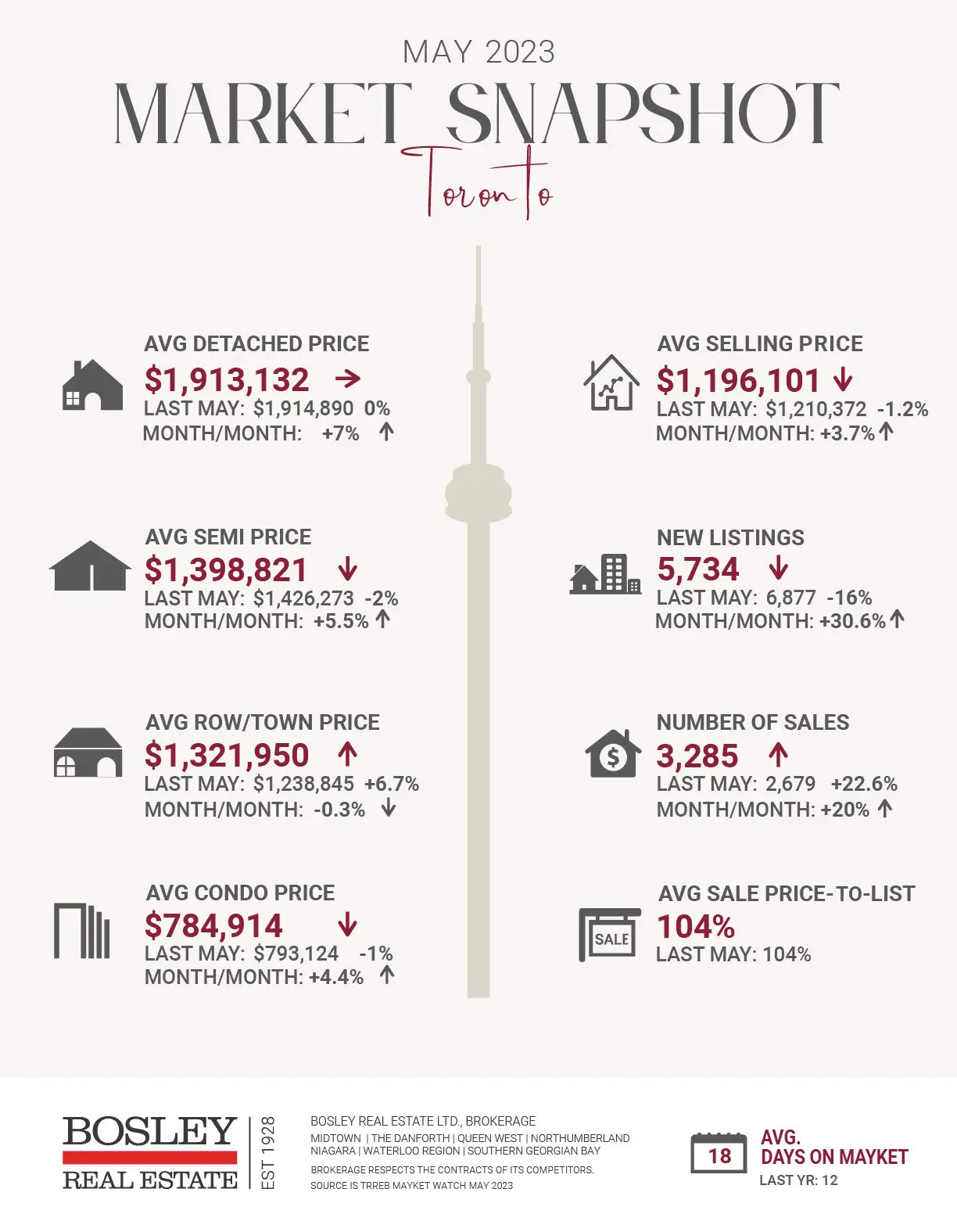

Canadian Banks Report 1 In 4 Mortgages Are 35 Years Or Longer.

Canadian first-time home buyers are 36 years old on average. That means they won’t have that starter condo paid off by the time they retire, according to recent bank reports. Four of the Big Five banks reported a large share of their portfolio had amortizations longer than 30 years in Q2 2023. Most of them have at least 35 years or longer remaining, as they extend terms to prevent over-leveraged buyers from defaulting.

An amortizing loan is one that’s gradually paid off over time, with each payment reducing the balance. Banks in Canada are limited to offering a maximum amortization of 30 years, meaning you have about 30 years to pay off the loan. Make your payments to cover the interest plus some principal, and you get close to zero. Straightforward, right?

In circumstances where the payment is insufficient to cover interest, it begins to accumulate. Rather than the balance getting closer to zero, it increases as time passes. This is called negative amortization, because the time required extends rather than winding down.

A combination of inadequate stress testing and poor regulatory control has led to a lot of negative amortizations. Despite being limited to 30 years at contract, banks estimate the “current customer payment basis” will be longer. Sometimes a lot longer.

A large share of the mortgage portfolios at Canadian banks have amortizations longer than 30 years. Leading is BMO (31% of its portfolio), followed by TD (27%), CIBC (27%), and RBC (26%). Only one of the Big Five proved to be an exception— Scotiabank at just 0.7% of its mortgage portfolio were amortizations of 30 years or longer. Many assumed it was a temporary issue last year and would resolve by Q2 2023. That wasn’t the case, with these banks only reporting slightly lower rates than last year.

The practice may not be an official thing in Canada, but it seems to have the regulator’s blessing. Earlier this month, OSFI ( Office of the Superintendent of Financial Institutions) wrote to Parliament to explain that removing the ability to extend mortgage amortizations might result in more delinquencies and create downward pressure on home prices.

It sounds noble to prevent defaults this way. However, existing owners are paying much less than average rents, and usually for a lot more space. Buyers

prior to 2021 also likely secured their home for significantly less than recent market prices. An increase in payment is unlikely to be burdensome to most, considering stress testing started in 2018.

That leaves recent buyers as the biggest group that needs these longer amortizations. While you might be thinking they’re first-time buyers that need a break, the odds are they’re investors. Over leveraged investors that can’t pay their mortgage and require special accommodations to prevent default sounds familiar, but it’s hard to remember where from.

Here are the top 5 trending stories of the week:

- Americans should be exempt from Canada’s foreign housing tax, members of Congress say “A bipartisan group of U.S. lawmakers is urging the State Department to ask that Americans be exempted from Canada’s tax on foreign property owners. The group has written to Secretary of State Antony Blinken to complain that Ottawa is unfairly punishing U.S. citizens who own vacation properties north of the border. “

- Hot Winters, Cool Springs: What Happened to Canada’s Seasonal Housing Cycle? “Once upon a time, Canada’s housing market had a very predictable annual cycle. Home sales were slow through the winter months, bottoming out in January, then would jump in the spring, hitting a peak in May and staying strong through the summer months, until they began a descent in the fall, back into the winter doldrums. ”

- Unlocking savings: A guide to government housing incentives to help your clients “Canadian first time home buyers are 36 years old on average. That means they won’t have that starter condo paid off by the time they retire, according to recent bank reports. Four of the Big Five banks reported a large share of their portfolio had amortizations longer than 30 years in Q2 2023. Most of them have at least 35 years or longer remaining, as they extend terms to prevent over-leveraged buyers from defaulting.”

- Unlocking savings: A guide to government housing incentives to help your clients “Homeownership can be expensive generally and in certain regions, particularly, not to mention daunting — especially for first-time buyers. As you help your clients navigate their way through the buying process, making them aware of the many housing programs and incentives available to help financially can offer some relief and reaffirm you as the expert advisor you are. “

- These Are the Top Features Canadian Buyers Want in a Home “Despite rising prices, Canadians still overwhelmingly desire detached suburban homes. To be specific, Canadians want contemporary single-family homes in the suburbs with three bedrooms, two bathrooms, an updated kitchen, outdoor space, and a garage.”

The Bosley Advantage

Read about the heritage and innovation that form the foundation for Bosley’s industry-leading approach to real estate.